Elon Is Paying 6% on Your Cash. The Math Says He Can't.

Every legitimate savings account in America prices below the Fed's rate. X Money sits above it. That gap is either a bribe or a breakthrough, and I think I know which.

The average savings account in America pays about 0.4%.

X Money, the payments platform Elon Musk began rolling out to verified users on June 25, pays 6%.

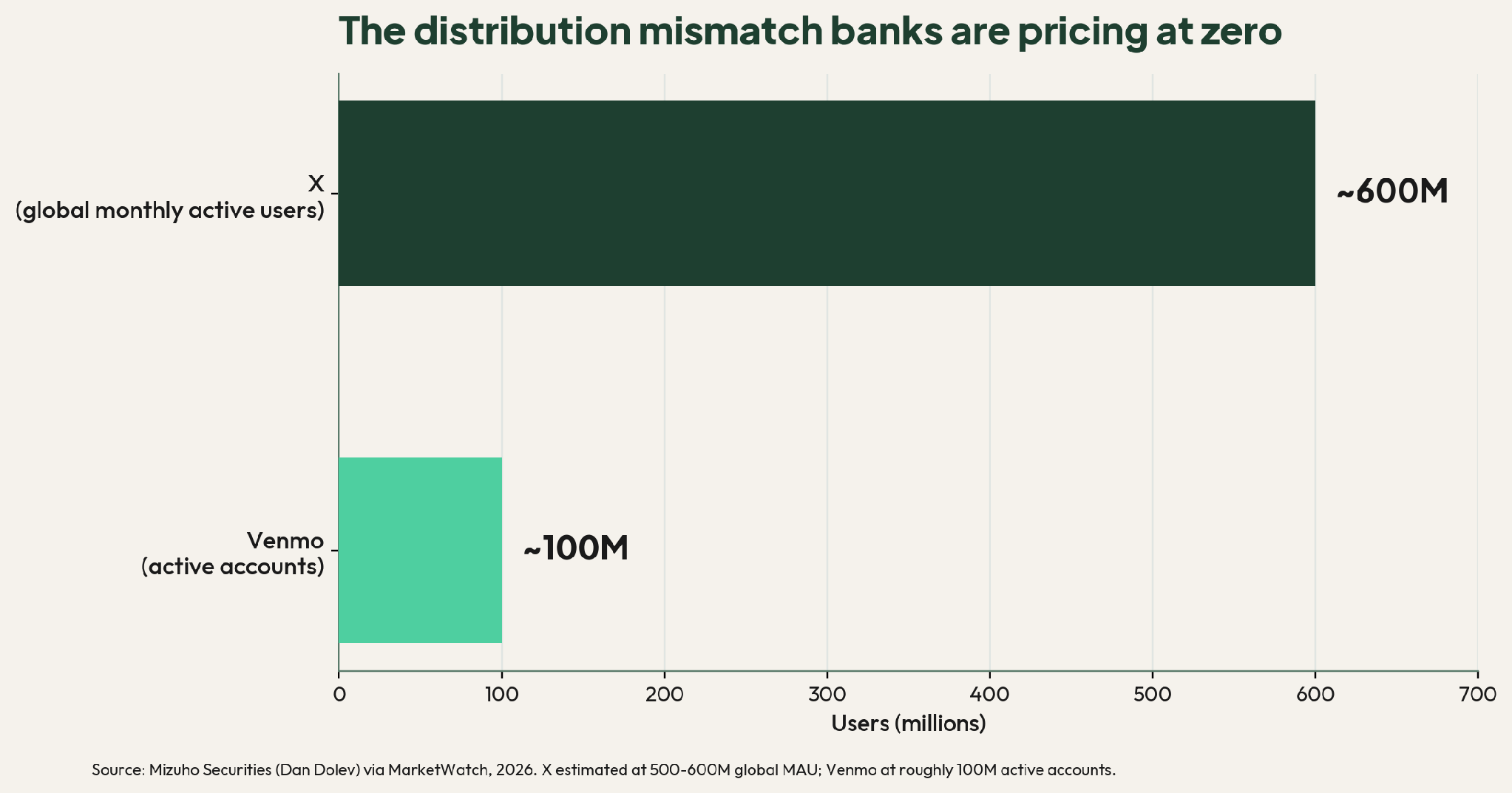

That’s the headline feature of a product that also includes a personalized metal Visa debit card, 3% cash back on purchases, zero foreign transaction fees, free ATM withdrawals, and peer-to-peer payments, all inside an app roughly 600 million people already open every day.

Deposits sit at Cross River Bank, an FDIC member out of Fort Lee, New Jersey, insured to $250,000 per depositor. Premium+ subscribers can reportedly extend coverage to $10 million through a sweep program that spreads balances across a network of partner banks.

• Up to $10 million of aggregate FDIC insurance coverage • Unlimited 3% cashback")

On paper, this is a fintech product launch, but in practice it might be the largest single idiosyncratic risk American retail banks have faced in decades.

The threat didn’t come through the front door. It came through the app.

The business model banks don’t want you to think about

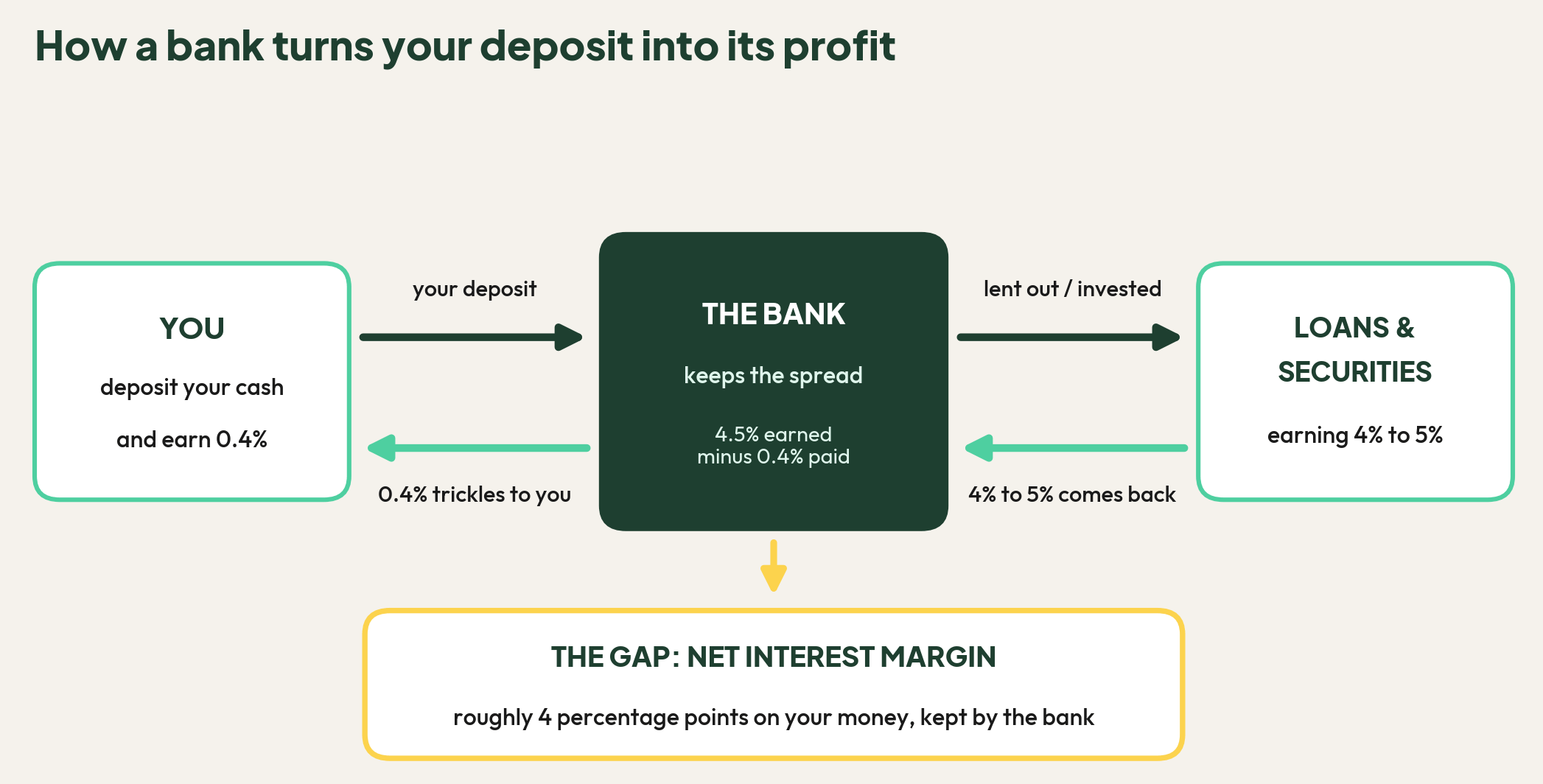

Here’s retail banking stripped to the studs.

You deposit money. The bank pays you almost nothing for it, lends it out or parks it in securities earning 4% or 5%, and keeps the difference. That gap is called net interest margin, and it’s the engine of the entire industry.

The engine runs on one assumption: you won’t move your money.

Inertia is the most profitable force in banking, and most Americans haven’t touched their primary checking relationship in over a decade. The industry counts on it.

Now put a 6% offer inside an app people check compulsively, attach it to a debit card with their handle engraved on it, and strip the friction out of switching. The target isn’t the saver who already ladders T-bills but the 28-year-old with $8,000 sitting in a megabank account earning nothing, who never opened a high-yield savings account because one never crossed their feed.

It’s crossing their feed now.

Everyone plays the yield game. Nobody has played it like this.

X didn’t invent the strategy of using yield to pry deposits loose. Fintech has run this play for a decade.

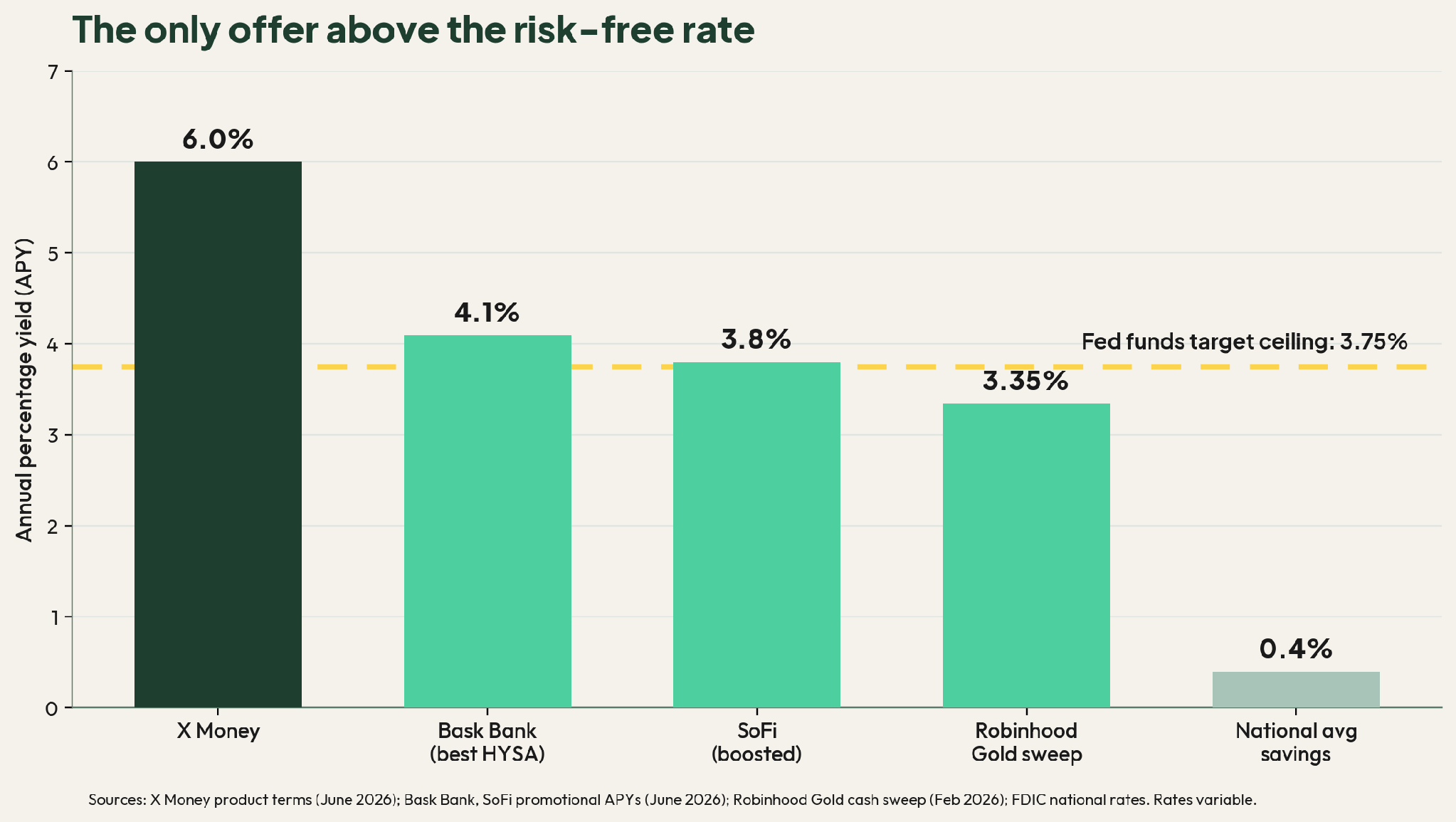

Robinhood Gold sweeps uninvested cash to partner banks at 3.35%.

SoFi pays up to 3.8% with a promotional boost.

Bask Bank, the strongest high-yield account in the USA right now, pays 4.1%.

Apple ran the same play with Goldman Sachs back in 2023.

Hold those numbers next to one more: the Fed’s target rate currently sits between 3.50% and 3.75%.

X Money is the only deposit offer in America priced above the risk-free rate. Every legitimate competitor sits below the gold line.

Every competitor prices below that ceiling, because that’s how deposit economics work. A bank earns roughly the risk-free rate on your cash, keeps a slice for itself, and passes the remainder to you.

X Money is the only offer above the line, and that single fact carries the whole story. Paying more on deposits than the risk-free rate returns means the product loses money on every dollar it gathers, unless those dollars are earning yield somewhere conventional banking doesn’t reach.

The fight the banks picked, and the punch they never saw

For the past year, the banking lobby has poured its energy into one battle: stopping stablecoin issuers from paying yield. The argument, made throughout the CLARITY Act debate, goes like this. If stablecoins can pay interest, deposits flee the banking system, credit creation suffers, and nonbanks end up running deposit operations without bank rules.

Credit where due: Carlo D’Angelo - The Stablecoin Strategist - made this observation before I did, and it reframed the whole fight for me. The banks spent their political capital guarding against yield-bearing stablecoins. Then X Money arrived paying 6% in plain fiat dollars, FDIC insurance included, and the stablecoin argument became beside the point.

The true path to digital asset adoption will come when user never touches a token. Whatever machinery hums in the background, what lands in the app is dollars, insured, spendable at more than 100 million Visa merchants.

It never mattered what generates the yield.

It mattered what the customer receives.

Distribution is the weapon. X’s user base is roughly six times the size of Venmo’s, with payments embedded in the daily habit rather than bolted onto it.

So where does the 6% come from?

Charlie Munger said it plainly in his 1995 Harvard speech on the psychology of human misjudgment: show me the incentive and I will show you the outcome.

A 6% liability has to be funded by something, and nobody at X has published the something. There’s no Truth in Savings disclosure, no disclosed minimum, and no rate history. I see 3 options for where/how this yield is generated:

It’s a marketing expense. X pays out more than the deposits earn and books the gap as customer acquisition cost. This is the oldest play in fintech, and nearly every teaser rate in the chart above came down once its growth target was hit.

It’s aggressive conventional banking. Cross River runs real lending operations and could sprint on a razor-thin margin to win volume. The chart says no. You can’t durably pay 225 basis points above the risk-free rate from a standard deposit-and-lend book. The math doesn’t clear.

The yield engine lives somewhere the depositor can’t see. X has publicly signaled crypto integration on the roadmap. Stablecoin reserves parked in T-bills throw off yield, and dollar-adjacent rails can be structured to produce returns that get paid out in fiat.

Here’s my view: The 6% starts as possibility one and, if the product survives, matures into possibility three. The subsidy buys the deposits, and the rails eventually fund the rate. That would mean X built the exact economic machine the banks tried to legislate away, wrapped it in FDIC insurance, and handed the customer a clean dollar balance.

This is a hypothesis, and I’ve labeled it as one, but it’s the only version of the story where the number on the front of the product ever stops burning money.

The Buffett Framework Question: Buffett has always favored businesses protected by high switching costs and customer inertia, and for decades retail banking was the textbook example. If a social platform can dissolve that inertia with a yield number and an engraved card, was the moat ever the banking relationship, or was it only the absence of a better offer inside the customer’s daily habit?

The Tell

A fair reading owes the skeptics their due.

Trust in money products is earned slowly, and X is asking people to hold savings inside the same app where they argue about politics. Venmo and Cash App spent a decade building credibility on narrow, boring use cases. Musk’s launch timelines have a habit of slipping, X Payments still holds no license in New York, Senator Warren’s letter is already on the record, and peer-to-peer payments inside a social graph is a fraud surface no traditional bank has to manage. Inertia has won nearly every one of these fights since 2010, which is why the fintech obituaries written for banks keep aging badly.

Grant all of it, and the test still runs. A nonbank with 600 million users is now measuring, in public, whether deposit inertia survives contact with a good enough offer delivered inside a daily habit.

👀 So here’s what I’d watch: The first rate cut.

The 6% is variable with no published terms, which means a cut is coming; the only questions are when and how deep.

A small trim, arriving slowly, says the engine is real and banks have a durable competitor paying near the risk-free rate with better distribution than any of them.

A fast, steep cut says this was a customer acquisition flare, the deposits reprice, and the industry exhales.

Either outcome answers the question the CLARITY fight never asked, which is whether the moat around bank deposits was the relationship itself or only the absence of a better offer.

My money says the rate falls and the deposits mostly stay.

Subsidies end. Habits don’t.

Have an awesome 4th of July Holiday fam! 🦅🇺🇸

Matthew Snider is the founder of Block3 Strategy Group, author of “Warren Buffett in a Web3 World,” and publisher of the BitFinance newsletter. He holds a Series 65 and MBA, and has been an active participant in digital asset markets since 2015. This article is for educational purposes only and should not be considered financial advice. Always consult with a qualified professional before making investment decisions.

Sources

Startup Fortune, “X Money rolls out to more verified users,” June 2026

TechTimes, “X Money Goes Live for Premium Users,” June 30, 2026

Forbes (Ron Shevlin), “Musk’s X Money: How It Could Win (And Why It Won’t),” April 2026

Bloomberg via Benzinga, early-access reports on 6% APY and 3% cash back, April 2026

Yahoo Finance, best high-yield savings accounts, June 2026 (Bask, SoFi rates)

Robinhood, High-Yield Cash Program APY (3.35% for Gold members), 2026