Tokenization’s Missing Buyers

Why tokenizing the right asset doesn’t matter if there’s no one set up to buy it.

A few days ago, Adam Blumberg published a piece in the Tokenized Asset Coalition’s Industry Veteran Series that did something the tokenization industry has spent five years avoiding.

It named the problem out loud.

Blumberg runs Protocol Wealth, an SEC-registered RIA built for the crypto-native ultra-high-net-worth investor. He has the clients. He has the conviction. He has six years of teaching this stuff before he ever launched the firm. Despite all of that, he can’t allocate to tokenized real-world assets in any meaningful way.

The reason isn’t skepticism. The piece is the opposite of skeptical, and that’s why I think it warrants consideration.

Somebody on the inside is saying out loud that the architecture being built right now will decide whether the trillion-dollar institutional channel ever shows up.

Here’s the part that landed hardest for me.

Walk into any conference that hgihlights “tokenization” today and you’ll hear the same pitches you heard five years ago:

Democratize access.

Bring smaller managers onchain.

Open up regional real estate, agricultural credit, specialty private credit, energy royalties, the long tail of strategies that traditional distribution couldn’t reach.

That’s it. That’s the only pitch that justifies the cost of building this industry.

What’s actually being shipped is tokenized share classes of the BlackRock USD Institutional Digital Liquidity Fund. Tokenized Apollo private credit. Tokenized Hamilton Lane. Tokenized KKR. Real funds, real institutions, real assets. None of that’s in dispute.

The question is whether tokenizing those funds advances the original case for tokenization at all. The answer is no.

Apollo and BlackRock and KKR were not assets that lacked distribution. An RIA who wanted Apollo private credit already had three different ways to get it. The tokenized version is a UI upgrade dressed up as a paradigm shift.

The original promise was about expanding the universe of managers who could compete for capital. The current path is a premium digital wrapper for the trillion-dollar managers who already had every distribution channel they needed.

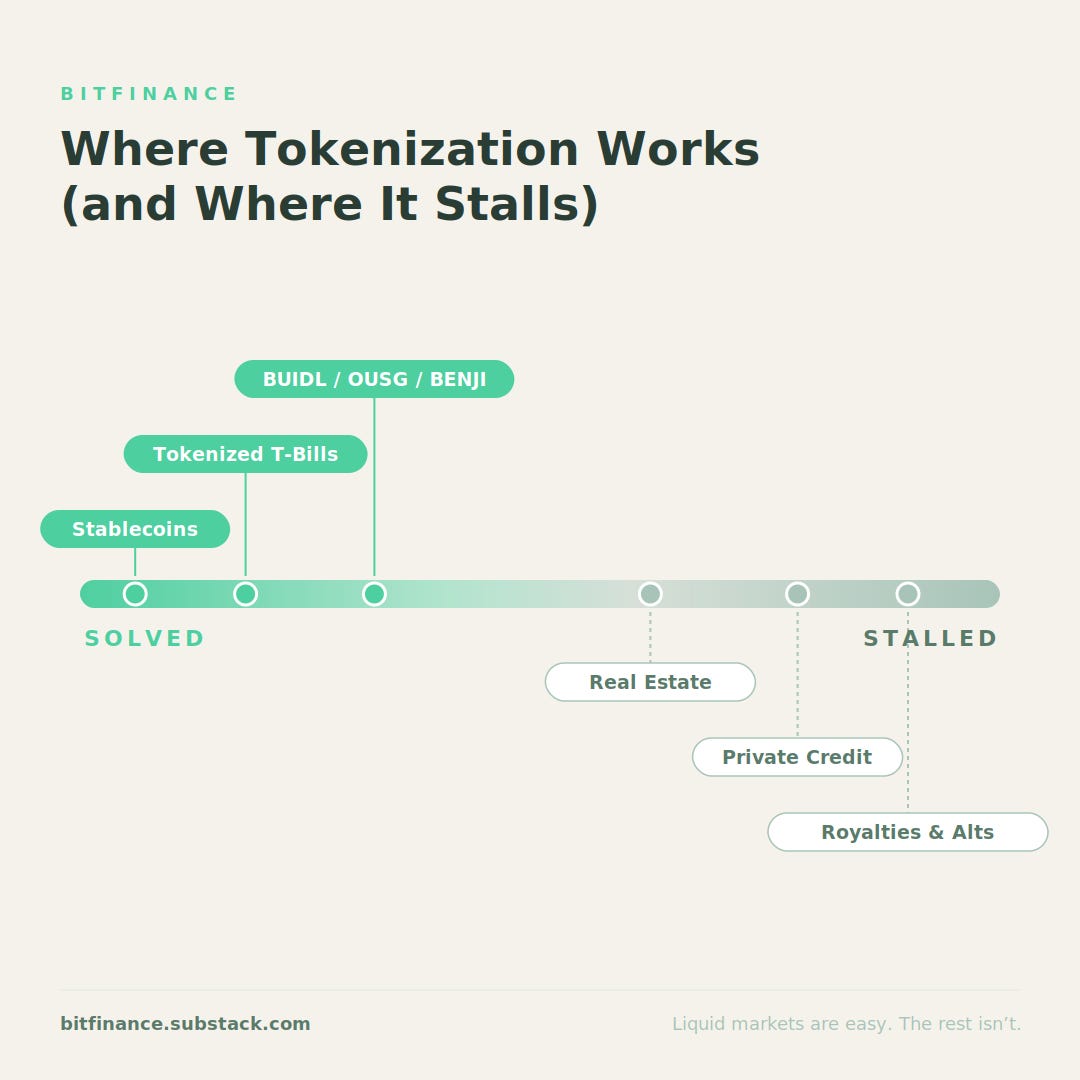

Where tokenization actually works

The bottom line is that tokenization works as a technology and foundation for transmitting value between parties when they would normally be illiquid.

The challenge, is that it’s worked in a narrow part of the market that most retail investors don’t think about as “tokenization” at all.

Let’s look at some examples:

Stablecoins are tokenized dollars. They work.

Tokenized Treasuries like BUIDL, OUSG, and BENJI are tokenized T-bills, and they’re growing fast because the underlying is homogeneous, the NAV is calculated by an established fund administrator, and the oracle just publishes a daily number.

The data tying the token to the asset is reliable, the income mechanics are clean enough to live with, and the use case (cash management onchain) is sharp.

That’s the easy case. Liquid underlying, transparent pricing, daily marks, simple income structure. Tokenization on liquid markets is largely a solved problem.

What hasn’t been solved is the case that actually justifies the regulatory complexity, the smart contract risk, and all the capital that’s gone into building this industry. Private credit. Real estate. Specialty finance. Royalty interests. Insurance-linked securities. The asset classes where the underlying economics are interesting precisely because the existing distribution machinery couldn’t reach them efficiently.

In those markets, tokenization runs into a problem that doesn’t show up in the marketing decks:

There’s nobody to buy what you’ve built.

The volume problem

Here’s the thing about tokenizing a private investment vehicle. The token can be perfectly designed. The smart contract can be flawless. The compliance modules can be elegant.

None of that matters if there’s no allocator on the other side ready to write a check.

In liquid markets, the buyers exist. Anyone with a stablecoin and a wallet can buy a tokenized Treasury. The market makes itself.

In illiquid markets, the buyers are fiduciaries managing other people’s money.

This means they have rules to follow requiring:

A qualified custodian that supports the specific token.

Verified accreditation that doesn’t require re-onboarding the client at every issuer.

The investment position to show up in their portfolio reporting system alongside everything else they manage.

A defensible answer to compliance about how income is delivered and how it gets taxed.

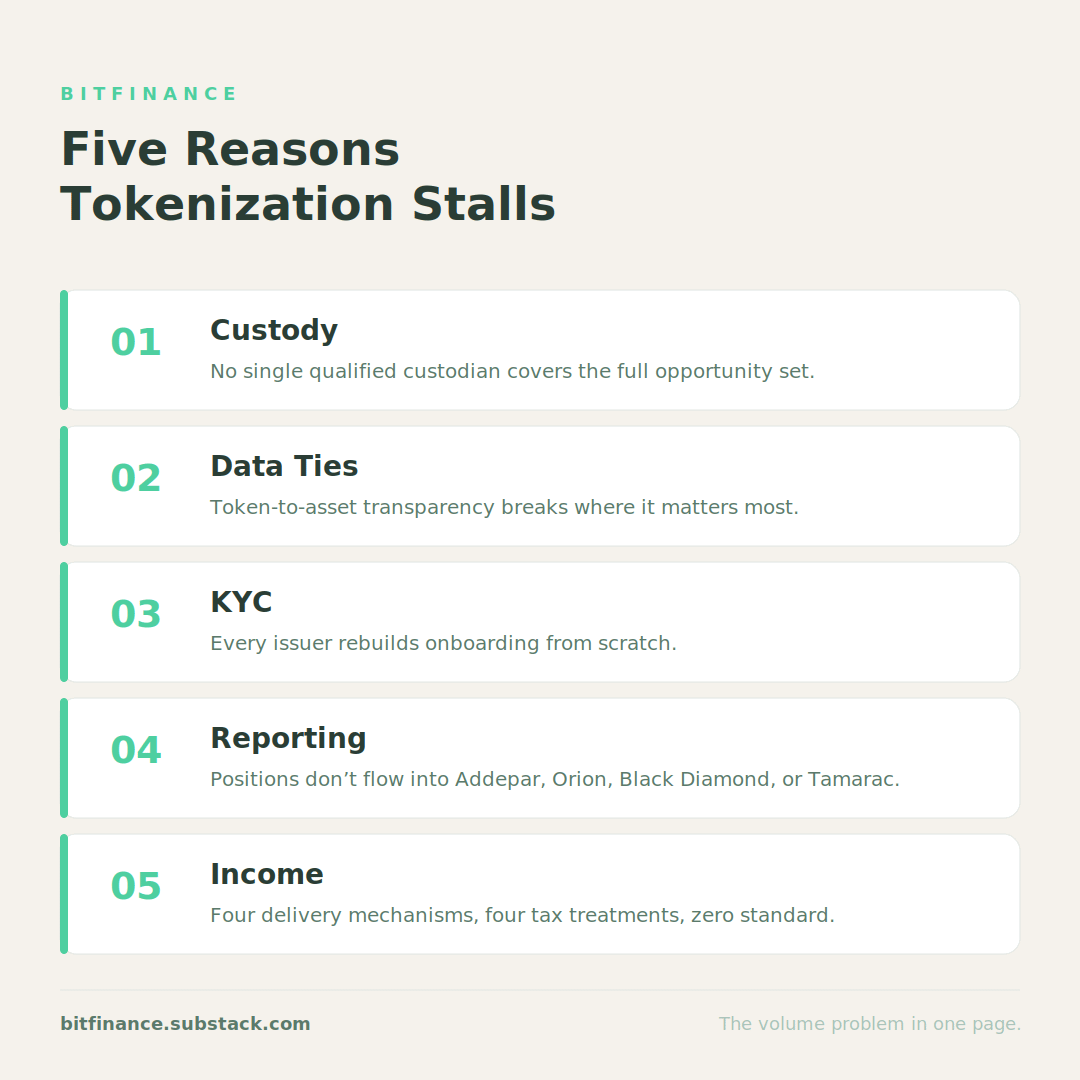

Blumberg lays out five operational reasons fiduciaries can’t currently buy tokenized alternative assets at scale.

Custody is fragmented across multiple platforms with no single coverage path.

Token-to-asset data is opaque exactly where it matters most.

KYC is rebuilt at every issuer.

Reporting doesn’t integrate with the platforms that actually run the wealth-management industry.

Income arrives through 4 different mechanisms with four different tax treatments.

None of those problems is technically intractable. All of them require infrastructure that crosses platform boundaries, and the platforms have been building inside their own walls instead.

And herein lies the rub:

you end up with tokenized regional real estate that nobody can allocate to.

Tokenized specialty private credit with low volume because the natural buyers can’t operationally hold it. The promise of tokenization, the one about reaching the manager you couldn’t reach before, dies at the operational layer.

Why this is on my desk

I’m in the middle of standing up a registered investment adviser in Puerto Rico. Part of the work I’m doing with that team is trying to engage this exact problem.

I don’t want to overclaim what we’re building. The infrastructure questions Blumberg names are coordination problems the whole industry has to solve together, and no single RIA is going to fix federated KYC or qualified custodian coverage on its own.

What I can say is that the gap between what tokenization promised and what it’s delivering is the central question I keep coming back to, and the firm I’m helping build is being designed with that gap in mind from day one.

The reason I’m telling you about this isn’t to pitch the RIA, but to make a point about what to watch for as the tokenization narrative gets louder over the next year.

As we progress, I’m excited to keep y’all apprised of the progress we make. The ultimate goal is to build a platform that can unlock many of the challenges we’re seeing related to volume and attract institutional players to participate.

In short…we’re hoping to build it so others will come.

What to watch

The tokenization headlines are going to keep coming. Larry Fink and Boston Consulting Group see this technology growing to tokenize tens of trillions of dollars worth of assets.

Every traditional asset manager will announce something. Every blockchain conference will have a tokenization track. The numbers being projected for tokenized RWAs by 2030 will keep climbing.

Most of that volume, if it materializes, will be tokenized versions of products that already existed.

Money market funds

Treasury products

Real estate

Share classes of institutional funds you could already access through a broker.

Useful incrementally for cash management and capital efficiency, but not the structural change in who gets to invest in what.

The structural change starts when the long-tail manager (the regional real estate operator with a track record, the specialty lender with differentiated underwriting, the niche credit shop you’d never have heard of through traditional channels) can actually find fiduciary buyers onchain. That requires operational infrastructure built across platform boundaries instead of deeper into single-platform silos.

It also requires fiduciaries to actually show up to participate, which is the slower part of the answer, and the part I’m spending my time on.

Tokenization is an unfinished experiment rather than a failed one.

The work that’s been done at the standards layer, at the custody layer, at the issuance layer is real and impressive. The work that hasn’t been done is the part that connects all of it into something a fiduciary can use to bring a new asset into a real client portfolio.

That gap is where the actual opportunity lives. It’s also where the next phase of this industry gets decided and I’m pumped to be building in a space like this!

Until next time!

Matthew Snider is the founder of Block3 Strategy Group, author of “Warren Buffett in a Web3 World,” and publisher of the BitFinance newsletter. He holds a Series 65 and MBA, and has been an active participant in digital asset markets since 2015. This article is for educational purposes only and should not be considered financial advice. Always consult with a qualified professional before making investment decisions.